Part 1

“Give all the power to the many, they will oppress the few. Give all the power to the few, they will oppress the many.”

— Alexander Hamilton

For nearly a decade, I have focused on identifying structural patterns within the international monetary system… signals that, at the time, were often dismissed or ignored.

Today, those same dynamics are no longer peripheral. They are moving to the center of the global stage.

Gold, once treated as a relic, is quietly re-emerging as a neutral reserve asset in a world increasingly defined by fragmentation, distrust, and competing power blocs.

At the same time, it is difficult to ignore the broader consequences of the modern monetary framework. The expansion of central banking, and the sustained growth of debt-based systems, has not operated in isolation. It has coincided with rising wealth inequality, increasing political polarization, and growing strain within the global order.

We are now witnessing a geopolitical environment that is arguably the most tense since the end of World War II.

At its core, this is not simply about economics.

It is about power.

Nations are no longer competing solely through traditional means. They are leveraging resources, supply chains, and financial infrastructure as tools of influence. Energy, metals, and critical minerals have become instruments of strategy—used to shape outcomes and redefine alliances.

Which raises a fundamental question:

How did these basic elements, resources known and valued for thousands of years, become so central to the balance of global power today?

Several forces appear to be converging:

1. Debt Expansion

The scale and persistence of global debt creation has distorted capital allocation, weakened currencies over time, and increased systemic fragility.

2. Resource Complacency in the West

Years of underinvestment—driven in part by policy, ESG frameworks, and regulatory constraints—have left many Western economies exposed when it comes to securing critical materials.

3. Strategic Industrial Policy in China

China has spent decades consolidating control across key resource supply chains. Through pricing pressure, state support, and long-term planning, it has positioned itself to dominate sectors where Western competitors have struggled to remain viable.

Over the past several years, I’ve grown increasingly frustrated with how fragmented and overlooked many of these big themes have been reduced to isolated headlines or lost entirely in the speed of modern media.

This piece marks the beginning of a series: The King on the Board: Gold and the Battle for Supremacy.

In the weeks ahead, I will examine, clearly and directly, the relationship between natural resources, sovereign debt, geopolitics, power, and central banking.

The objective is simple:

To connect the dots behind a system that is changing in real time.

In future parts of this series, I will go further back.

But for the purpose of this opening piece, it is important to begin with a defining moment: the 2008 global financial crisis.

This was a period when the global financial system came dangerously close to seizing entirely, placing trillions in assets, and the savings of millions, at risk.

At the center of the crisis was the widespread mispricing and distribution of mortgage-backed securities. What had been presented as stable financial instruments ultimately exposed deep structural fragilities within the banking system.

The result was severe strain across major institutions, with several collapsing outright and others requiring extraordinary intervention to survive.

The day Ben Bernanke moved to stabilize the financial system marked a turning point not just for markets, but for the structure of money itself.

Faced with cascading failures across major financial institutions, the Federal Reserve intervened with unprecedented force. Liquidity was injected at scale, interest rates were rapidly cut, and emergency facilities were introduced to prevent a complete collapse of credit markets.

What followed was the beginning of a new era.

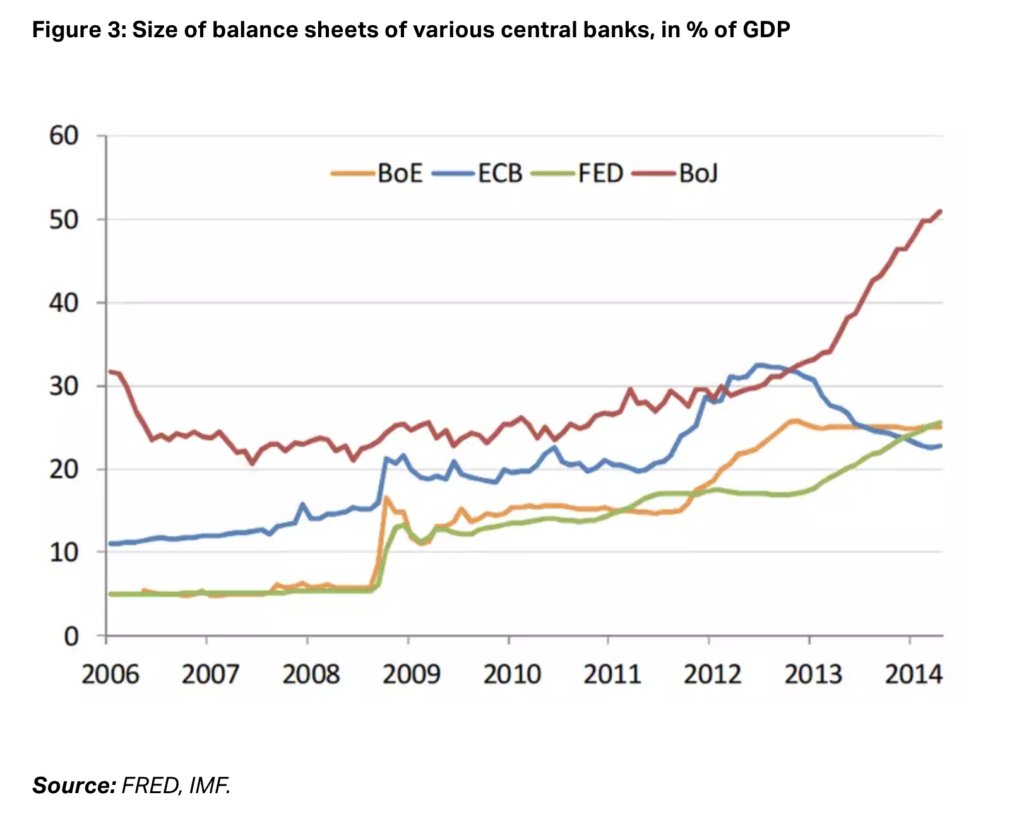

Quantitative easing, once considered extraordinary, became embedded policy. Central bank balance sheets expanded at a pace never before seen. The cost of money was pushed toward zero, distorting risk, incentivizing leverage, and reshaping capital allocation across the global economy.

In the immediate term, the system was stabilized.

But in doing so, the foundation was fundamentally altered.

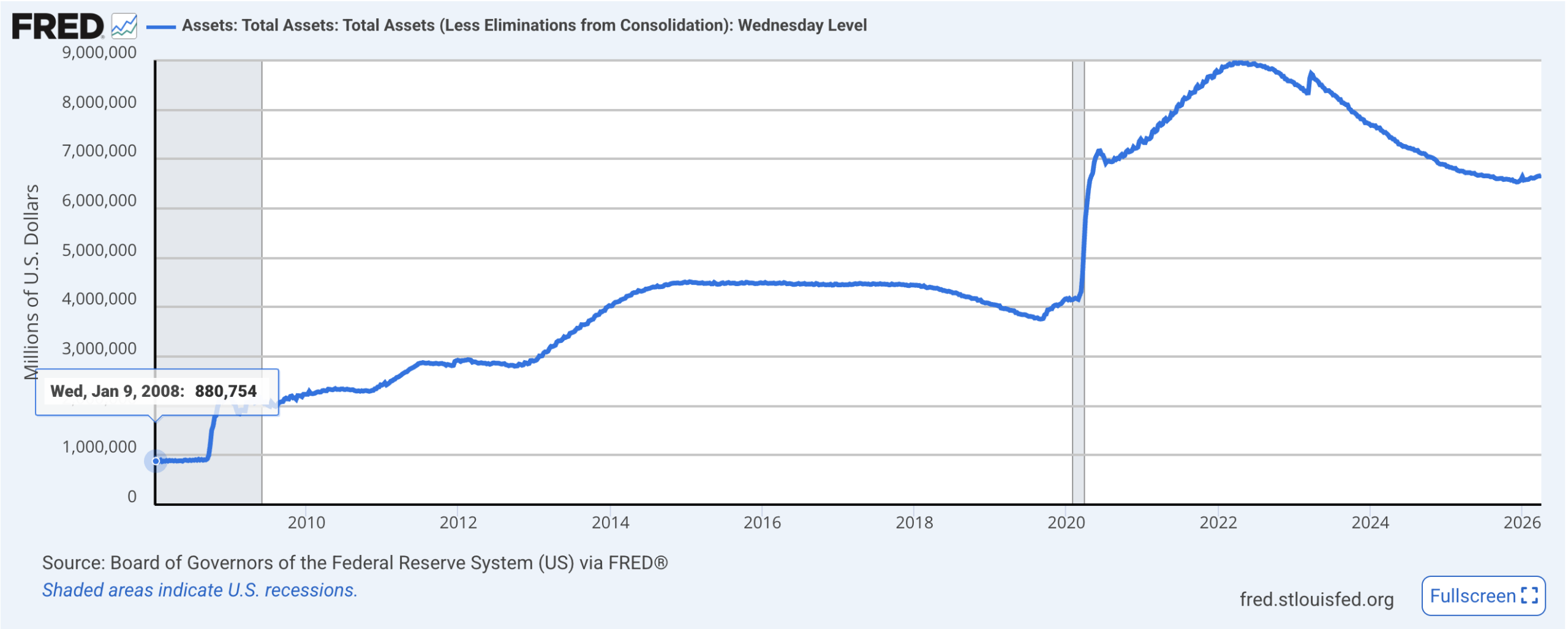

If you had told anyone in 2008 that the balance sheet of the Federal Reserve would expand from under $1 trillion to more than $6.5 trillion, it would have been dismissed as unimaginable.

Yet over time, what began as an emergency response became a defining feature of the modern financial system.

What is often forgotten is that the crisis did not remain contained within the United States.

It exported instability across the global system.

European banks deeply exposed to U.S. credit markets faced severe stress. Institutions such as Royal Bank of Scotland and UBS required massive support after suffering heavy losses tied to mortgage-backed securities.

Interbank lending froze. Dollar funding markets seized. Even fundamentally sound economies found themselves cut off from liquidity.

What began as a U.S. housing crisis quickly became a global liquidity crisis.

And in doing so, it revealed a critical truth:

The financial system was far more interconnected and far more fragile than most had understood.

China Enters the Picture

In the aftermath of the crisis, as the scale of U.S. intervention became clear, Chinese policymakers began openly questioning the stability of a system anchored to a single national currency.

In March 2009, Zhou Xiaochuan then governor of the People’s Bank of China called for a new international reserve currency independent of any single nation.

His proposal centered on expanding the role of IMF Special Drawing Rights.

But the message was broader.

China was signaling a lack of confidence in the long-term stability of the dollar-based system.

At the time, the idea was dismissed.

In hindsight, it marked an early signal that major powers were beginning to reassess the foundations of the global monetary order.

Fast forward to today, and that reassessment is no longer theoretical it is beginning to materialize.

Across the world, we are seeing early signs of de-dollarization from bilateral trade agreements to alternative settlement systems.

But this shift is not happening in isolation.

It is unfolding alongside a deeper structural consequence of the post-2008 monetary response.

Since the crisis, policies led by the Federal Reserve including near-zero interest rates and quantitative easing have been heavily oriented toward supporting asset prices.

In the short term, this stabilized the system.

But over time, it reshaped its outcomes.

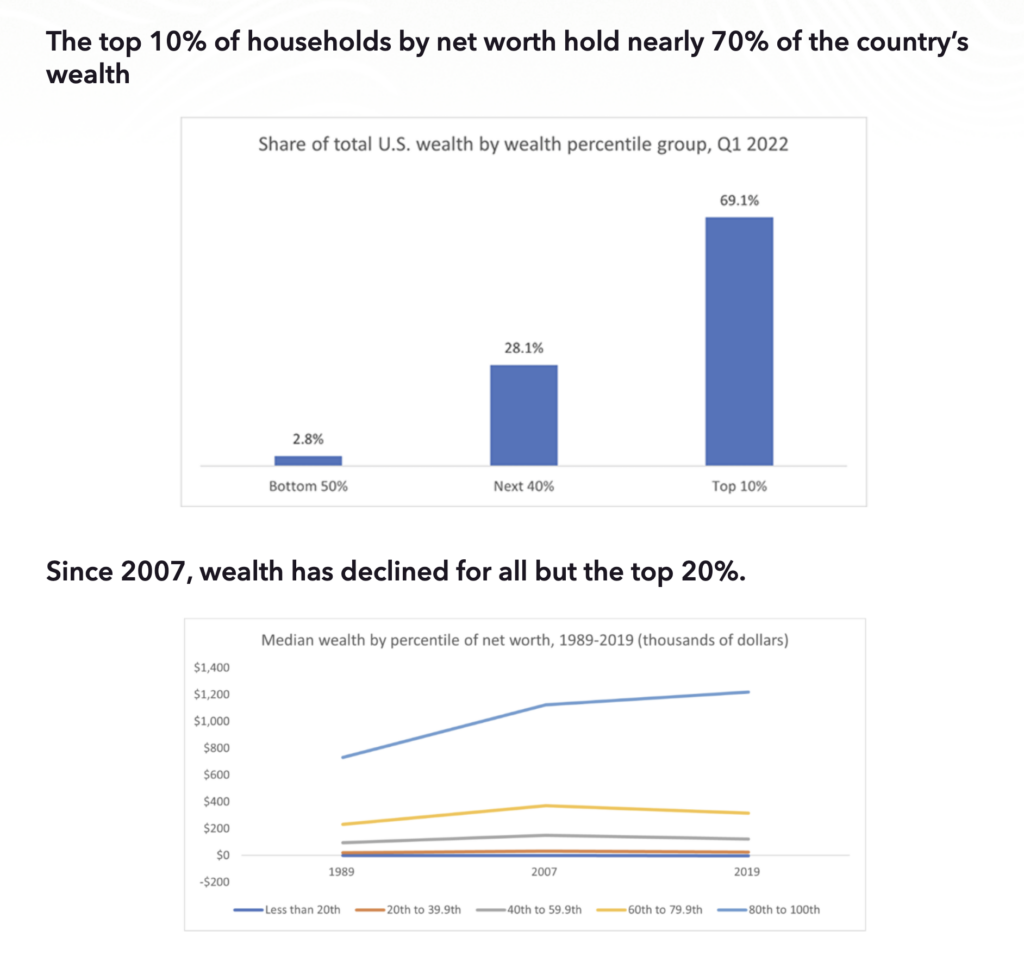

Financial assets, equities, real estate, and other risk assets have appreciated significantly, disproportionately benefiting those who already owned them. While wages have grown in nominal terms, they have generally lagged behind the pace of asset inflation and, in many cases, struggled to keep up with the rising cost of living.

The result has been a widening gap between those with access to assets and those without.

This is not simply a social issue.

It is a structural one.

When monetary policy consistently prioritizes asset inflation, it reinforces a system where capital is rewarded over labor, and access to financial markets becomes a key determinant of economic mobility.

Over time, this dynamic feeds into broader consequences: political polarization, declining trust in institutions, and increasing pressure on the existing order.

And this is where the connection becomes clear.

As internal imbalances build within the system, external confidence begins to fracture.

The Return of Gold as Monetary Infrastructure

And in that vacuum of trust, something else is quietly returning.

For decades, gold was treated as a hedge… useful in times of stress, but largely minor to the functioning of the financial system itself.

That framing is beginning to shift.

In recent years, central banks have been buying gold at the fastest pace in modern history.

Countries are repatriating reserves, moving physical metal back within their own borders. At the same time, there are growing signs that price discovery is no longer confined to Western exchanges alone.

Even at the policy level, ideas once considered fringe by the mainstream… gold-linked instruments, convertibility frameworks are re-entering the conversation.

This is not about returning to the past.

It is about what happens when confidence in the existing system begins to erode.

Gold, in that context, is no longer just an asset.

It begins to look like infrastructure.

China’s Role with Gold

China’s approach to gold is defined less by what is disclosed and more by what is deliberately left unsaid.

Official reserve figures released by the People’s Bank of China show a steady increase in holdings in recent years. Yet, across markets and policy circles, there is broad skepticism that these figures capture the full extent of China’s accumulation.

Historically, major powers have treated gold as a strategic asset closely held and rarely transparent. In that context, China’s opacity is not an anomaly it is a message.

What is more revealing is the infrastructure China has built alongside its accumulation.

The development of the Shanghai Gold Exchange has helped establish an alternative center for gold trading, one more closely tied to physical delivery and domestic metal flows than Western futures-driven markets. Over time, this divergence has raised questions about where true pricing power ultimately resides.

At the same time, China has steadily linked gold to its broader financial strategy.

The internationalization of the yuan, the expansion of cross-border payment systems, and bilateral trade increasingly conducted outside the dollar all point in the same direction: a gradual reconfiguration of monetary influence.

China is not simply diversifying reserves.

It is building optionality to support its currency, to influence settlement, and to participate in a system where gold plays a larger role.

This possibility has not gone unnoticed in the West.

Kwasi Kwarteng once raised the prospect that China could eventually anchor its currency to gold arguing that, under the right conditions, such a system could form the basis of a more stable international monetary order.

What once appeared speculative now carries more weight.

Because the question is no longer whether the system is changing.

It is who is preparing for that change and who is not.

The Weaponization of Commodities

At the same time, the role of commodities is changing.

Resources are no longer just economic inputs they are tools of statecraft.

Roughly a fifth of the world’s oil flows through the Strait of Hormuz. Control over LNG, uranium, copper, and other critical materials is increasingly shaping geopolitical strategy.

Export controls, once rare, are now being deployed with growing frequency. Governments are restricting the flow of key materials and technologies to protect domestic industries and exert leverage abroad.

Sanctions are met with countermeasures. Supply chains are redirected. What was once built for efficiency is now being reshaped for resilience and control.

In the 20th century, conflict was defined by territory.

In the 21st, it is increasingly defined by supply chains.

The Fragmentation of the Dollar System

Against this backdrop, the monetary system itself is beginning to shift.

Not through collapse but through gradual fragmentation.

The dollar remains dominant. But its share of global reserves is declining at the margins. Trade is increasingly being conducted in local currencies. Alternative settlement rails are emerging.

What is forming is not a replacement system but a parallel one.

A multi-rail structure where the dollar remains central, but no longer uncontested.

And within that shift, another big message is becoming increasingly difficult to ignore.

Central banks are accumulating gold at a pace not seen in decades as I previously mentioned.

In fact, recent data shows that the value of gold held by central banks has now surpassed their holdings of U.S. Treasuries marking a structural shift in how reserves are being allocated.

This is not a rejection of the system.

But it is a hedge against it.

Taken together, these shifts point to something deeper.

A change in how trust is formed.

A change in how value is stored.

A change in how power is exercised.

This is not a reset that will be announced.

It is a transition already underway—quietly, unevenly, and increasingly visible to those paying attention.

And if history is any guide, by the time it is fully recognized…

it will already be too late to position for it.